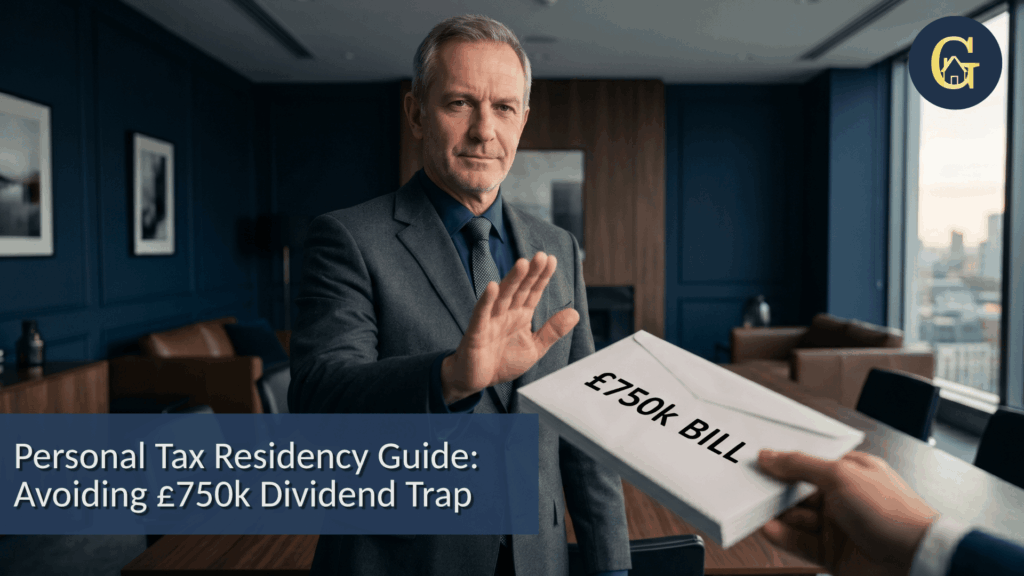

Imagine this: You have spent years building a successful UK trading business or property portfolio. You decide it is finally time to reap the rewards, move to Dubai, and enjoy a tax-efficient lifestyle. You plan to withdraw a £1 million dividend from your UK company, expecting to pay 0% tax in the UAE. But six months later, HMRC knocks on your door with a tax bill for nearly £750,000.

For many entrepreneurs and investors, this isn’t a hypothetical nightmare, it is a reality caused by a misunderstanding of Personal Tax Residency UK rules. At GoldHouse Accounting, we believe that true financial freedom comes from clarity. This guide will help you navigate the complexities of the 2026 tax landscape so you can protect your family wealth and focus on your legacy.

Understanding Personal Tax Residency vs. Simply “Living Abroad”

Many people believe that “leaving the UK” is as simple as packing a suitcase and spending most of your time in the sun. In reality, Personal Tax Residency UK is a formal legal status determined by HMRC, and it is entirely possible to be “living” in Dubai while remaining a UK tax resident in the eyes of the law.

The most common trap is the “90-day fallacy.” We often speak with expats who believe that as long as they spend fewer than 90 days in the UK, they are “safe.” Unfortunately, it isn’t that simple. Without a formal change in status and a clear break under the Statutory Residence Test (SRT) 2026, HMRC may still consider you a resident. If you are deemed a UK personal tax resident, you are liable for UK tax on your worldwide income, no matter where in the world you earned it. Whether you are seeking expert accounting for landlords or looking for ways to mitigate property tax UK, your residency status is the foundation of your entire strategy.

The 2026 Dividend Sting: Why HMRC is “Hammering” Non-Residents

The financial stakes have never been higher. Let’s look at the math: If you take a £1 million dividend while HMRC considers you a UK resident, your tax bill would be approximately £373,925. However, the “sting” goes further. Because the tax exceeds £1,000, you are hit with “payments on account” – effectively paying for next year’s tax in advance. This can double your immediate liability to nearly £747,850.

In 2026, the situation is even more critical. New regulations mean that non-UK residents can no longer claim certain notional tax credits on UK dividends, making the “hammering” even more severe for those who fail to plan their Dubai business setup or UK exit correctly. This creates a massive cash flow crisis, potentially draining 75% of your payout instantly.

The Statutory Residence Test (SRT): The Deciding Factor

To avoid this trap, you must master the Statutory Residence Test (SRT) 2026. This is the only framework HMRC uses to decide your status, and it rests on three pillars: the Automatic Overseas Test, the Automatic UK Test and the Sufficient Ties Test.

One of the biggest dangers is the “Home” test. If you keep a home available to you in the UK for at least 30 days, you could trigger automatic UK residency, regardless of how many days you spent abroad. Many property investors fall into this trap by leaving a “base” in the UK for visits. At GoldHouse, we often advise clients on how to sever these ties – for example, by ensuring a formal rental agreement is in place so the property is no longer “available” for their use. Furthermore, for the year you actually move, you must correctly apply for “split-year treatment” to ensure your income is protected from the moment you leave.

The “Sufficient Ties” Test & The 5-Year Temporary Residency Rule

If you don’t meet the automatic tests, HMRC looks at your “ties” to the UK. These include family ties, accommodation, work and the 90-day tie. The more ties you have, the fewer days you are allowed to spend in the UK without being considered a resident.

Crucially, you must be aware of the Temporary Non-Residence Rules HMRC. If you move abroad, take a large dividend and then return to the UK within five years, HMRC can retrospectively tax that income as if you never left. In an era of Making Tax Digital, HMRC’s ability to track your movements is more precise than ever. Rigorous compliance and digital logging are no longer optional – they are essential for protecting your wealth.

Professional Exit Planning: Your 9-Year Strategy

Effective UK Expat Tax Exit Planning is not a one-time event; it is a long-term strategy. A true change in residency requires a 9-year outlook:

- Analysing the 3 years before you leave,

- The year of departure

- The 5 years you remain abroad to avoid the temporary residency trap.

Because definitions like “what counts as a work day” are subjective and highly scrutinised, a professional SRT assessment is the only way to safeguard a business exit or large dividend. Whether you are optimising a SSAS pension or scaling a global business, our Asset consultancy ensures your transition is seamless.

Secure Your Global Legacy with GoldHouse

Navigating the intersection of UK and Dubai tax laws requires more than just a standard accountant; it requires a strategic partner who understands the ambitions of entrepreneurs and property developers. At GoldHouse Accounting, we provide the clarity you need to move forward with confidence.

By working with us, you gain more than just tax savings – you gain time freedom, reduced stress and the peace of mind that your family’s legacy is secure. Let us handle the complexities of HMRC while you focus on building your future.

Ready to secure your financial freedom? Contact GoldHouse Accounting today for a specialist residency assessment.